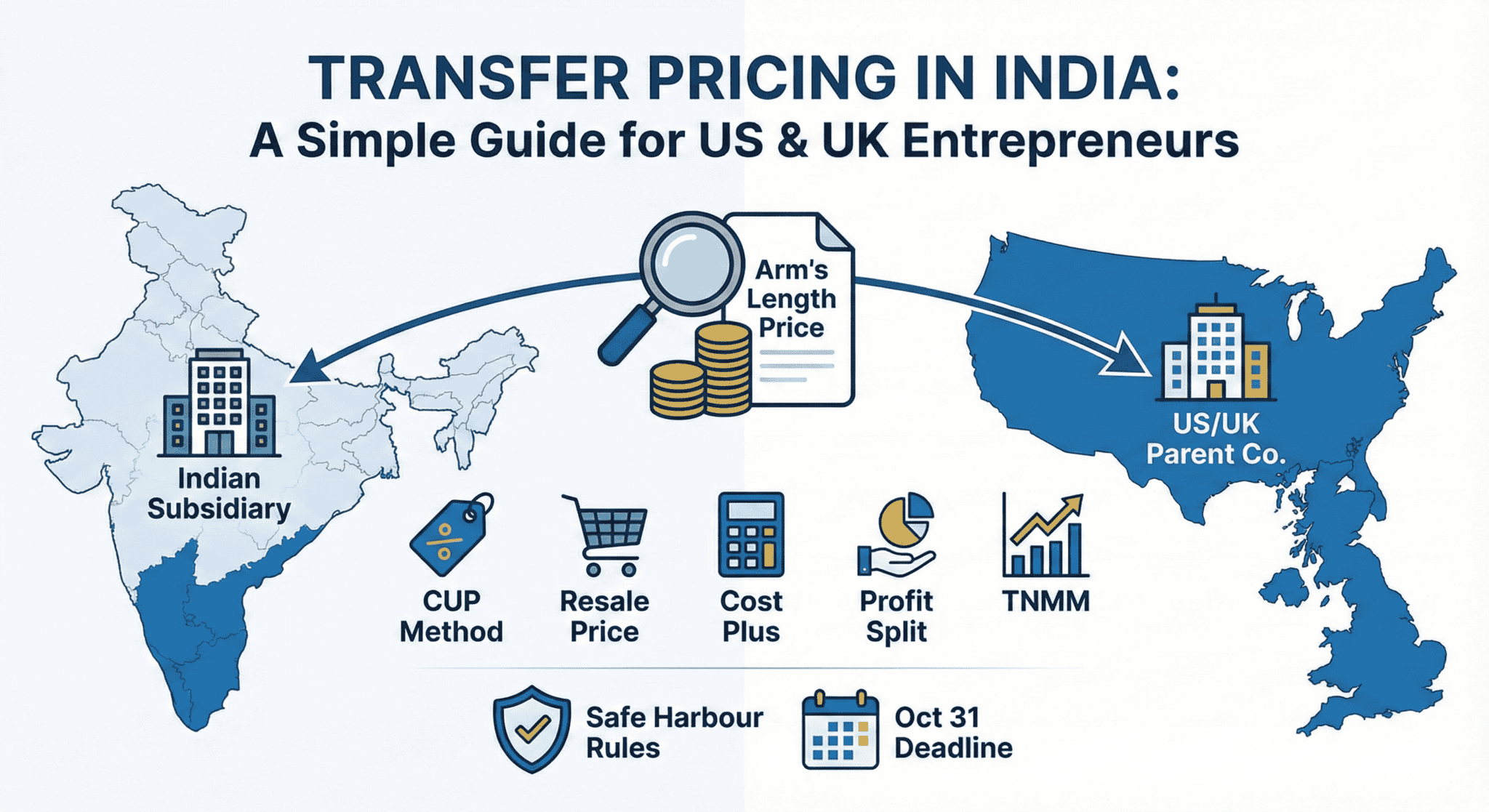

Are you a US or UK entrepreneur expanding into India? Congratulations. You are entering one of the world’s most dynamic markets. However, as you set up your subsidiary, you will face a complex tax concept called Transfer Pricing (TP).

Don’t worry. As a Chartered Accountant helping global companies like yours, I will explain this simply. Think of this as your “plain English” guide to staying compliant and profitable.

Table of Contents

ToggleWhat is Transfer Pricing? (The “Pizza” Example)

Imagine you own a pizza chain. Your parent company is in the UK, and you open a subsidiary in India.

The UK parent company sells the secret “dough mix” to the Indian subsidiary. What price should you charge for that dough?

If you charge too high, the Indian company makes zero profit (and pays zero tax in India).

If you charge too low, the UK company loses money, but the Indian company makes a huge profit.

Indian tax authorities want to ensure you don’t charge “too high” just to shift profits out of India. Transfer Pricing is simply the set of rules that forces you to price that dough fairly, as if you were selling it to a stranger.

Why Does India Care?

India’s corporate tax rate for foreign companies has historically been 40% (plus surcharges), though recent budget proposals aim to reduce this to 35%. In contrast, domestic Indian subsidiaries often pay between 15% and 25%.

Because these rates might be higher than in the UK or parts of the US, the Indian taxman worries you will shift profits abroad to pay less tax. Therefore, strict TP regulations exist to stop this “Base Erosion.”

The Golden Rule: Arm’s Length Price (ALP)

Every transaction between your overseas parent and Indian subsidiary must be at an Arm’s Length Price (ALP).

Simple Definition: The price you would charge a complete stranger for the same product or service.

If you sell software to your Indian team for $100, but you sell it to a third-party client for $150, the tax officer will tax you on $150. Consequently, you must prove your price is fair.

The 5 Transfer Pricing Methods (Simplified)

How do you calculate this “fair price”? The Indian government allows five main methods. You must choose the one that fits your business best.

1. Comparable Uncontrolled Price (CUP) Method

Best for: Commodities or simple products.

How it works: You compare your price directly to a market price.

Example: You sell a generic microchip to your Indian unit for $10. The market price for that chip is $10. Match! You are safe.

2. Resale Price Method (RPM)

Best for: Distributors/Resellers.

How it works: You look at the final sale price and work backward, subtracting a standard profit margin.

Example: Your Indian unit buys perfume from your UK HQ and sells it to Indian customers for $100. If standard distributors make a 20% margin, the transfer price should be roughly $80.

3. Cost Plus Method (CPM)

Best for: Manufacturers or Service Providers.

How it works: You calculate your direct costs and add a standard industry markup.

Example: Your Indian team writes code for the US parent. It costs them $50/hour to run the office. If the industry standard markup is 15%, you must pay them $57.50/hour.

4. Profit Split Method (PSM)

Best for: Complex partnerships where both sides contribute unique value (like joint R&D).

How it works: You split the total global profit based on who did what.

5. Transactional Net Margin Method (TNMM)

Best for: Most IT and Service companies (Most Popular).

How it works: Instead of looking at product prices, you look at net profit margins.

Example: Your Indian subsidiary provides back-office support. You compare its net profit margin (e.g., 12%) against other independent Indian back-office companies. If they also make 12%, you are compliant.

The “Safe Harbour”: A Zero-Headache Zone

Does this sound complicated? Fortunately, India offers a shortcut called Safe Harbour Rules.

If you agree to declare a certain profit margin, the tax authorities promise not to audit your transfer pricing. It acts as a peace of mind fee.

Current Safe Harbour Thresholds (FY 2024-25 estimates):

Software Development / IT Services: If you declare an operating margin of 17% to 18% (depending on turnover), you are safe.

KPO Services: Margins between 18% and 24%.

Corporate Guarantees: 1% fee per annum.

However, you must officially “opt-in” for this scheme. It is not automatic.

Critical Compliance Deadlines

You cannot just set the price and forget it. You must document it.

Form 3CEB (The Audit Report):

You must hire a Chartered Accountant to certify your transactions were at Arm’s Length.Deadline: October 31st every year.

Penalty: ₹100,000 for non-filing.

TP Documentation (Local File):

If your international transactions exceed ₹1 Crore (approx. $120,000), you must maintain a detailed study report (TP Study).Penalty: 2% of the total value of transactions. This can be huge!

Master File:

For larger global groups (Turnover > ₹500 Crore), you must file detailed global structure forms.

Conclusion

Transfer pricing in India is strict, but it is manageable. The key takeaways are:

Always transact at an Arm’s Length Price.

Choose the right method (TNMM is common for services).

Consider Safe Harbour rules to avoid litigation.

Never miss the October 31st filing deadline.

Do these rules apply if my Indian company makes a loss?

Yes. In fact, loss-making subsidiaries attract more attention. The tax officer will assume you are undercharging the parent company to create artificial losses in India.

Can I just use the same transfer price I use in China or Vietnam?

No. India requires a specific “India-centric” benchmarking study. You must compare your Indian unit with other Indian companies, not global averages.Yes. In fact, loss-making subsidiaries attract more attention. The tax officer will assume you are undercharging the parent company to create artificial losses in India.

What is the penalty if I don't maintain documentation?

The penalty is severe. It is 2% of the value of the international transaction. If you transferred $1 million, the fine is $20,000—just for missing paperwork.

Rohit Lohade is a Chartered Accountant and India entry specialist at KRPR & Associates. With 15+ years of experience, he has assisted 250+ international companies — including global brands — incorporate and operate in India. He currently serves as Resident Director for multiple foreign-owned Indian subsidiaries.